5 Ways Seniors Can Get the Most Out of Social Security Benefits

Dec 9, 2024

Do you want to know how to get the most out of your Social Security benefits when you retire? The first thing you must do is arm yourself with information.

As partial replacement income, Social Security benefits are critical in retirement planning. The amount you get monthly can spell the difference between being financially secure and only getting by when you finally stop working.

In this article, learn more about claiming benefits early versus waiting until full retirement age.

1. Make the Most Out of Your Primary Benefits Through Work and Timing

There are two things you need to take full advantage of your Social Security h when you retire – timing and work years.

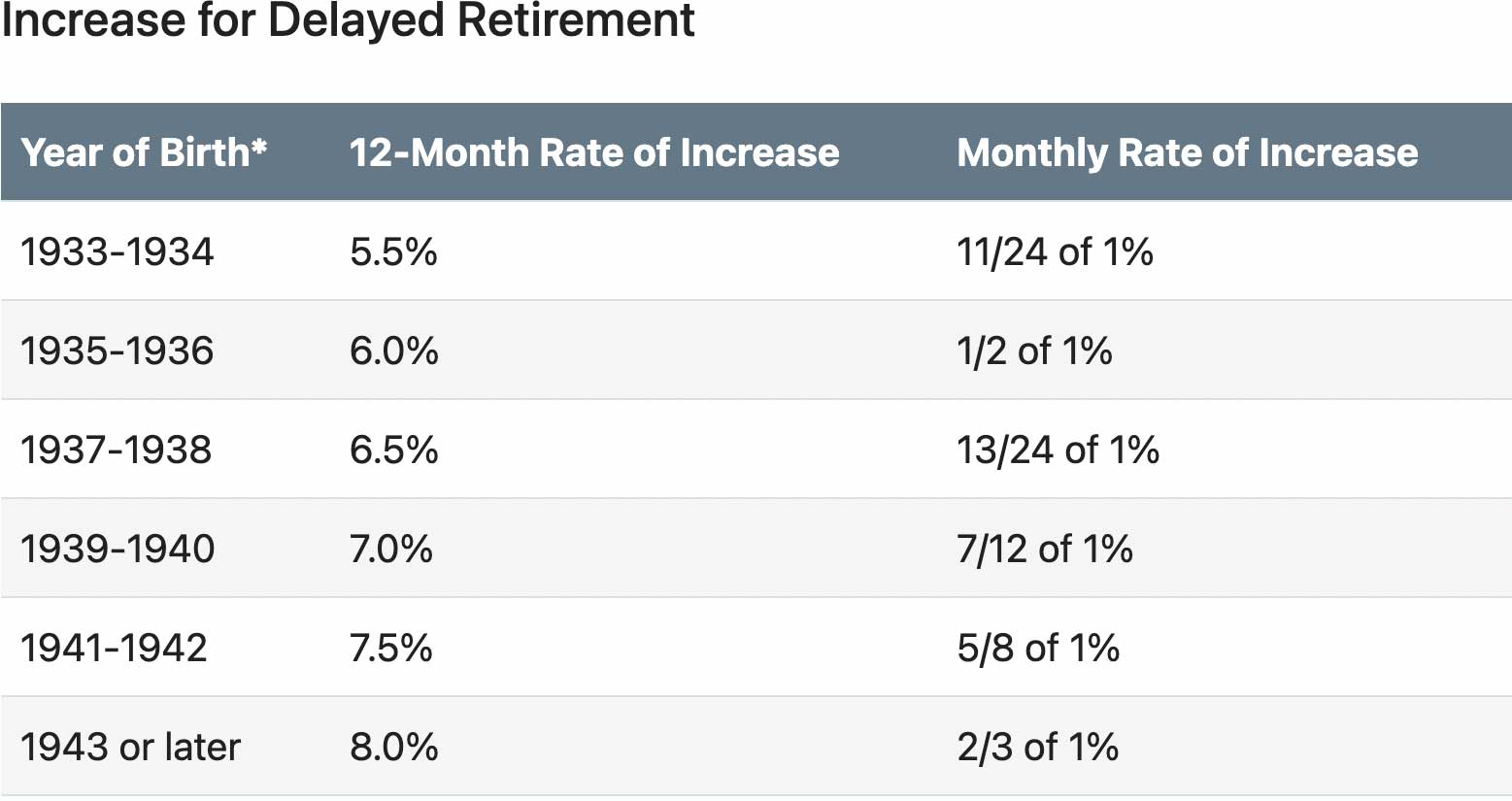

So, if you’re still employed, rack up at least 35 years of employment or work until your full retirement age. Then, wait to claim your Social Security benefits until your 70th birthday.

The Social Security Administration grants delayed retirement credits for beneficiaries who wait until after they reach full retirement age to claim their benefits.

Check out the chart below to see the increase you might get for delayed retirement.

2. Consider Collecting Spousal Benefits

There are several considerations when you want to avail yourself of spousal benefits and they include the following:

- You and your spouse were born before January 2, 1954

- You both worked for at least 35 years (though you are eligible after 10, know that the benefits will be lower)

- You are both at full retirement age (your eligibility starts at 62, but the PIA at this age is lower)

Eligible married individuals can file a “restricted application.” This means forgoing claiming their own Social Security benefits, but instead collecting the retirement benefits based on their spouse’s total work earnings.

Although you can switch back at any time once you’ve done this, the best approach would be to wait until you’re 70 to acquire the most delayed retirement credits.

You may still qualify for spousal benefits if born after January 2, 1954. However, you must go through “deemed filing,” which requires you to apply for your benefits and that of your spouse all at once. In cases like this, you will be granted the one with the higher lifetime benefit amount.

It might be wise to claim spousal benefits if you are married and one is significantly earning more than the other.

3. Look Into Claiming Survivor Benefits

If you survived the death of a spouse, you may qualify for monthly survivor benefits. The amount for this is based on the earnings of the deceased employee.

You will get the maximum benefits at the full retirement age of 66 if you were born between 1945 and 1956. This retirement age increases to 67 if you were born in 1962 or later.

As you can see, the full retirement age for survivor benefits is not the same for retirement benefits. However, if you want to claim earlier, you can collect reduced benefits when you reach 60. If you have a disability, you can claim as early as 50.

Suppose you already collected your own Social Security benefits and want to claim survivor benefits. In that case, the Social Security Administration will check if you can get a bigger amount as a surviving spouse.

If you can, you will receive a combination of benefits equivalent to the higher amount. You must apply to switch to survivor benefits and submit your spouse’s death certificate.

To apply or learn more about survivor benefits, click here.

4. Combine Social Security Benefits With Pension Plans

Combining your Social Security benefits with your pension can make you financially secure. A pension plan is one of the most reliable sources of retirement income, allowing you to enjoy life and manage your expenses as a retiree.

However, certain provisions can affect your primary insurance amount or leave you with no Social Security benefits. A “non-covered pension” can cut down your retirement benefits through either the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO).

There are ways these two provisions won't affect your benefit amount, though, and you'll find them below.

Ways these provisions won’t cut down your benefits

- You have a railroad pension

- Your wages not covered by Federal Insurance Contributions Act (FICA) taxes were from before 1957

- You were hired to work for the federal government in 1984 or later

- You were employed for at least 30 years by companies that paid FICA taxes

- You worked for a non-profit organization exempt from paying FICA taxes on December 31, 1983, and you meet other conditions

Also, the GPO won’t impact your benefits if:

- You have a government pension from work covered by FICA taxes and you meet one of a few other qualifications

- You qualified for a government pension before December 1982 and were deemed eligible for spousal benefits under provisions enacted in January 1977

- You have a government pension not based on your work wages

- You worked for the federal government, switched from the Civil Service Retirement System to the Federal Employees Retirement System after December 31, 1987, and you meet one of several other requirements

- You qualified or were granted a government pension before July 1, 1983, and received one-half spousal support

5. Merge Your Social Security With Your Retirement Savings

Make proportional withdrawals if you have multiple retirement savings accounts like 401(k), Individual Retirement Account (IRA), or other retirement plans. Establish a target income amount and withdraw a percentage from each account based on your total savings.

This tactic will help you get a more stable tax bill when you retire. It can even reduce your lifetime taxes and increase your income after taxes.

If you have a traditional IRA, it’s also smart to convert your funds to a Roth to help lessen your taxable income when you retire. Also, it’s ideal that you withdraw more from your Roth. This strategy will help prevent a Social Security “tax torpedo,” wherein as much as 85% of your benefits become taxable.

Your income from your retirement savings accounts will not impact your Social Security retirement benefits but will affect the taxability of these monthly payouts. However, if your income is less than $25,000 or $32,000 if you filed jointly with your spouse, you won’t have to pay taxes on your benefits.

Plan for the Future With a Comprehensive Retirement Plan

Knowing the impact of claiming benefits when you’ve reached full retirement age or even waiting until you’re 70 can spell the difference between living well and getting by.

So, evaluate your situation and understand it well. This plan will allow you to create a comprehensive retirement plan that includes your Social Security benefits.

If you have already worked for 35 years, take advantage of claiming spousal benefits and delaying benefits. Also, consider how to lower the taxes on your retiree's income.

Lastly, work with a financial planner who can help you create a plan. A reliable financial advisor will guide you in integrating your Social Security benefits with other retirement savings accounts and income sources. With them by your side, you will be set up for life and can enjoy your retirement.